Healthcare Isn’t Optional

Ben Franklin once said that “two things in life are certain: death and taxes.” If we were to add a third, it would be people needing healthcare before they pass on.

Modern first world countries increasingly see healthcare as a right, not a luxury or discretionary service.

The healthcare real estate market is already large and diversified; recent estimates place the broader U.S. healthcare real estate market size at over $1.3 trillion, growing at roughly 6–7% annually in the years ahead. (Grand View Research).

With over 4M Baby Boomers turning 80 within the next five years, medical real estate is uniquely positioned to capitalize on the healthcare demand that this growing cohort, one of the most active users of medical real estate, desperately needs.

With operational complexities and regulatory hurdles, this asset class, like any investment, is not immune to risk, which we’ll discuss in detail in this whitepaper.

This paper is not intended to persuade; it’s intended to provide a critical review that investors can use to determine if a meaningful capital allocation to this asset class makes sense for their portfolio.

What Exactly Is Medical Real Estate?

At its core, medical real estate houses licensed providers delivering essential healthcare services. This distinction from other CRE types, like office, retail, and multifamily, has practical implications.

Patients engage with these facilities because care is required, not because economic conditions are favorable. That underpins much of the durability associated with medical real estate.

In practice, it consists of 4 main categories:

Medical Office Buildings (MOBs): Facilities housing physician practices, diagnostics, and outpatient services, often located near hospitals or dense population centers and leased under longer-term agreements.

Urgent Care, ER’s and Specialty Clinics (Including Micro-Hospitals): Standalone or retail-adjacent facilities providing episodic or specialized services such as urgent care, imaging, dialysis, or ambulatory surgery.

Post-Acute and Long-Term Care Facilities: Including skilled nursing, assisted living, and hospice properties, which introduce additional operational and regulatory considerations and are often evaluated separately.

Hospital and Health System Campuses: Inpatient and outpatient facilities, frequently surrounded by affiliated MOBs and specialty clinics, that anchor regional healthcare delivery.

Recent Macroeconomic Trends

Over the past ten years, some third-party analyses have reported strong total returns for segments of medical real estate relative to broader benchmarks (results vary; past performance is not indicative of future results). Here’s why.

Demand for this asset class is shaped less by economic cycles and more by long-term demographic and clinical realities that evolve over decades.

Inflation, interest rates, and labor costs still matter but what differentiates medical real estate is that these pressures interact with non-discretionary demand, creating a fundamentally different risk profile than traditional property types.

The following sections focus on the structural trends most relevant today:

- ✓Aging Demographics

- ✓Population Imbalances

- ✓Increasing Longevity

- ✓The Shift Toward Outpatient Care

As you’ll see, these are not just the demand drivers that have historically supported medical real estate’s relative outperformance; they’re also likely to persist.

Trend #1

The Population is Aging

The most powerful driver of demand for medical real estate is the rapid aging of the US population.

In order to understand just how pervasive this trend is, take a look at this chart from the World Economic Forum:

This graphic analyzes US Census data to highlight three trends:

1. The population is expanding.

2. The average age of men and women is getting older.

3. People are expected to live even longer.

We’ll expand on the last two datapoints in the next section, but the first one warrants a further explanation.

As the population increases, the demand curve for everything goes up and to the right. That means there’s more demand for haircuts, sandwiches, and, of course, medical real estate.

Population ↑

Average Age ↑

Life Expectancy ↑

Trend #2

Life Expectancy is Increasing

Diseases that were once fatal are now chronic.

Procedures that once required long hospital stays are now performed on an outpatient basis.

Early detection has become more precise, more routine, and more widely accessible.

Advances in medical technology, pharmaceuticals, diagnostics, and preventative care have meaningfully extended both lifespan and the number of years individuals live with managed, treatable conditions.

This is also reflected in the data. In 1960, life expectancy was 69.8 years for both men and women. Today, it’s grown to 78.4 years.

Life Expectancy

Trend #3

Baby Boomers are Entering Retirement

The term “Baby Boomer” is not a metaphor; it is a demographic fact.

Between 1946 and 1964, the United States experienced an unprecedented surge in births following World War II. This cohort grew larger than any generation before or since, earning its name because of the sheer volume of people born during that period.

Take a look at the chart below, where you can see data collected from the CDC on the number of expected births per woman for each generation:

Source: CDC

By 2030, the entire baby boomer generation will be of retirement age, expanding the share of adults 65 and older to ~20% of the population, up from 17% in 2024.

This shift is not gradual at the margins; it is a large, visible wave moving into the years of highest healthcare utilization.

Older age cohorts account for a disproportionately large share of medical visits, procedures, diagnostics, and ongoing treatment.

As a result, healthcare demand does not simply increase in line with population growth; it accelerates as this generation ages. CBRE estimates that outpatient healthcare spending alone is expected to increase by more than 30% over this period, driven primarily by aging demographics and the continued shift toward non-hospital care settings.

Trend #4

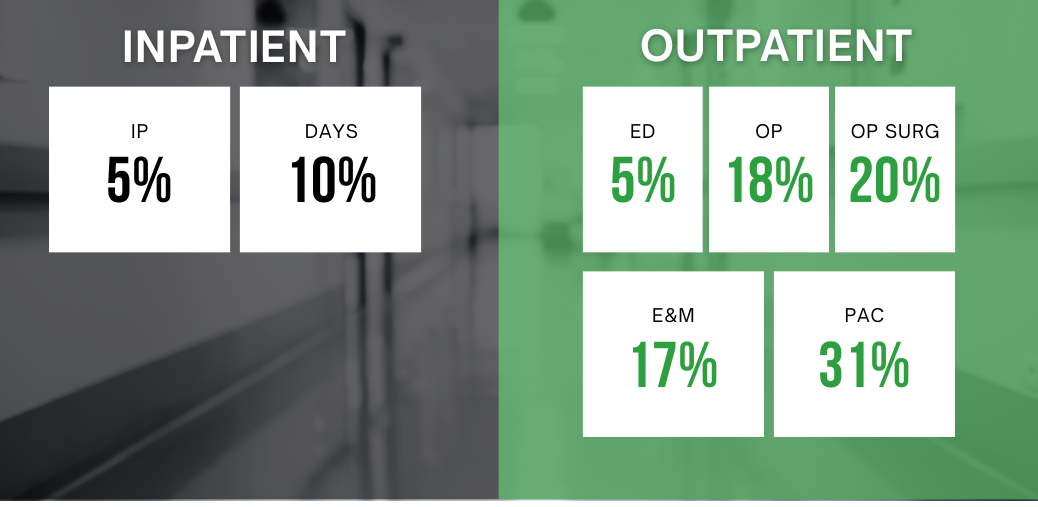

Outpatient Services are Growing in Demand

Over the past decade, the center of gravity in U.S. healthcare delivery has shifted away from centralized inpatient settings toward outpatient environments. (In laymen’s terms, “outpatient settings” do not require a hospital check-in).

This evolution reflects a combination of clinical advances, cost considerations, and patient preference, rather than a single policy or market cycle.

Data from Sg2, a Vizient company specializing in analytics, backs this up:

Common Misconceptions

Despite these strengths, misconceptions persist that can lead to poor allocation decisions:

“All medical real estate is the same.”

It is not. Subtypes (outpatient buildings, urgent care, dialysis centers, specialty surgical facilities) each have different demand drivers and tenant risk profiles.

“Higher rents always translate to better performance.”

Rising rents in certain markets reflect scarcity, not universal strength. Effective underwriting must separate structural demand from local supply constraints.

“Healthcare facilities are recession-proof.”

They are resilient, but not impervious. A severe economic shock can affect patients’ ability to pay out-of-pocket costs, insurers’ reimbursement behavior, and provider expansion plans.

Good investment in this sector is not about chasing yield; it is about understanding tenant credit quality, demographic tailwinds, lease structure, and service delivery models that ultimately anchor the real estate value.

Direct Assessment of Risks

Medical real estate carries risks, not the least of which is reliance on the healthcare ecosystem itself.

Tenant risk: If a large medical practice fails or consolidates, the landlord must manage retenanting. This requires underwriting beyond real estate into healthcare economics.

Regulatory risk: Changes in reimbursement policy can affect providers’ economics, indirectly influencing their ability to meet lease obligations.

Supply concerns: In some markets, new construction could catch up with demand, creating downward pressure on rents and occupancy.

But these are real risks, not theoretical ones, and informed investors calibrate underwriting accordingly. Rigorous due diligence should include analysis of local demand drivers, provider concentration, payer mix, and service utilization patterns.

Why This Asset Class Works Especially Well for Direct Ownership

Medical real estate aligns uniquely with long-term, income-oriented capital:

Cash flow: Outpatient and medical office leases often run long and are structured to pass expenses through to the tenant, reducing landlord burden.

Demographic alignment: Aging populations are a bullish structural input independent of economic cycles.

Operational simplicity: Many medical real estate assets are leased on a triple-net (NNN) basis, shifting responsibility for taxes, insurance, and maintenance to the tenant. Combined with longer lease terms and lower tenant turnover, this structure reduces day-to-day management burden and creates clearer, more predictable cash flow for owners compared with traditional office or retail properties.

For investors interested in durable cash flows, this combination of robust demand, absolute NNN leases (where the tenant typically bears most operating costs, subject to lease exceptions and owner obligations), and essential services make medical real estate an attractive option.

Summary: 5 Takeaways

Below are 5 clear, fundamentals-driven reasons medical real estate (particularly outpatient and medical office assets) continues to stand apart from traditional commercial property types.

Healthcare demand is non-discretionary. Patients seek care because it’s required, not because economic conditions are favorable, creating demand that is far less sensitive to business cycles.

Aging demographics create a multi-decade demand tailwind. By 2030, adults aged 65+ will represent roughly 20% of the U.S. population, up from 17% in 2024. Older age cohorts consume a disproportionately large share of healthcare services, accelerating demand rather than merely sustaining it.

Life expectancy continues to rise. U.S. life expectancy has increased from 69.8 years in 1960 to 78.4 years today. Advances in diagnostics, pharmaceuticals, and preventative care mean more people live longer with chronic, managed conditions, driving recurring medical visits and space utilization.

Outpatient care is structurally replacing inpatient care. Healthcare delivery has steadily shifted away from centralized hospitals toward outpatient settings such as medical office buildings, imaging centers, and ambulatory surgery facilities, expanding demand for specialized, off-campus medical real estate.

Medical tenants are highly “sticky.” Medical practices invest heavily in tenant-specific buildouts, licensing, and local patient relationships. These sunk costs discourage relocation, leading to lower turnover and longer average lease durations (to the tune of 7-15+ years) compared to traditional office tenants.

Closing Reflection

Medical real estate doesn’t trade on sentiment, technological hype, or short-term narratives. Its demand is not consumer discretionary or fashion-driven.

Its strength lies in something far more durable: human need.

The trends discussed in this whitepaper are structural realities shaping how, and where, care is delivered. As medicine evolves toward outpatient settings and long-term condition management, the physical infrastructure supporting that care becomes increasingly essential.

For investors, this means medical real estate does not depend on perfect timing or aggressive assumptions. Its demand is anchored in necessity, not novelty. That doesn’t eliminate risk, but it does provide important context for the asset class as a whole.

Success in this asset class is less about predicting the next cycle and more about underwriting fundamentals that persist regardless of market sentiment.

For those seeking long-duration cash flow, operational clarity, and alignment with unavoidable demographic trends, medical real estate earns its place as a core component of a thoughtfully constructed real asset portfolio.

About Custom Capital

Custom Capital is a private family office founded by Jason Milton and Patrick Truhlar.

We’re focused on helping investors acquire high-quality commercial real estate aligned with long-term structural demand.

Over the past three years, Custom Capital has assisted its clientele in acquiring nearly $500 million in commercial real estate across multiple asset classes, with a particular emphasis on absolute NNN properties with long average lease lengths.

Our approach is guided by extensive deal sourcing. We allocate over $250,000 a month to help investors find commercial properties aligned with their needs.

Jason Milton

CEO Founder

Patrick Truhlar

COO

This whitepaper is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities or investment products. The information presented reflects general market observations, assumptions, and third-party data believed to be reliable but not independently verified and subject to change.

Custom Capital does not provide investment, legal, tax, or accounting advice and does not act as a fiduciary, investment adviser, broker-dealer, or fund manager. Any transaction, if pursued, is structured as an arms-length sale of real property interests and is governed solely by definitive legal documentation. All investments involve risk, and no guarantees of performance, cash flow, tax outcomes, or results are made.